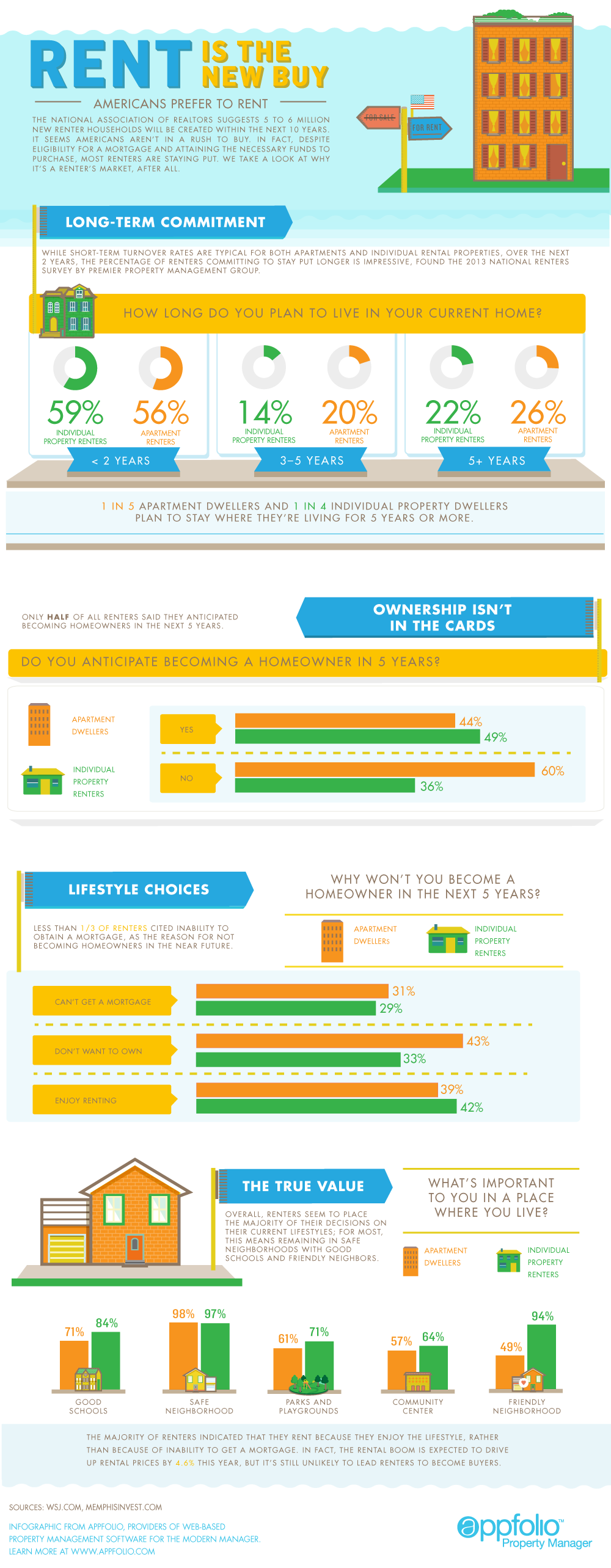

Source: AppFolio.com

Nearly 7 years after the financial crisis of 2008, a time when mortgages seemed available to almost any American, the “American Dream” of owning a home continues to fade.

The “old” dream was to save enough money for a down payment on a home that you could own or partly own by qualifying for a mortgage that you could pay off over time. Times have really changed.

First of all, although mortgage interest rates had dipped to historic lows after the financial crisis, qualifying for a mortgage became a more daunting task as standards tightened in the aftermath.

The interest rate on a 30-year, fixed rate mortgage recently jumped from 3.87% to 4.04% the week ended June 11. That’s the highest level since October 2014 and followed a correction in Treasury bonds. The 10 year Treasury bond yield is the benchmark for setting rates on 30-year mortgages.

If the Federal Reserve decides to begin raising short-term interest rates for the first time since the financial crisis, mortgage rates may move even higher. This exacerbates the largest cost of home ownership…debt maintenance.

The media recently suggested that mortgage rates are heading towards 5% in the months ahead. Some industry pundits suggest even higher rates will unfold over time.

Mortgage rates haven’t been at the 5% level since early in 2011. That spike put a temporary damper on home buying activity and by November 2012 the 30-year rate plunged as low as 3.31%.

Rising rates matter. The Mortgage Bankers Association on June 10 said refinance applications during the previous week fell nearly 9% from just a month before and had fallen 4.8% from a year ago.

While owning a home comes with certain advantages, it comes with a number of onerous drawbacks. First, the buyer has to tie up around 20% or more of the price of the house for the down payment.

As one investment analyst stated, “The carrying costs – what’s needed to hold and maintain the asset – range from property taxes and home insurance to emergency repairs and renovations.”

In many states the average annual property taxes range from as low as 1.3% to as high as 5% of the assessed valuation. Often the sales price ends up being the updated value for tax assessment purposes.

On a house that sells for $300,000 in an area with property taxes on the low end of the scale (for example purposes I’m using 1.5%), the annual tax hit of $4,500 is a hefty amount.

Add up the other costs of home ownership that are above-and-beyond the amount of principle and interest owed each month for the mortgage and suddenly the “dream” looks more like a nightmare!

As the cost of buying and maintaining a home continues to climb the advantages of renting are likely to shine brightly.